Has Disney Walked Into Its Own Trap ?

Today's Fun Fact

Academy Awards for Best Animated Feature films were first given in 2001 to Shrek.

Here's what you need to know before the US markets open.

What to expect in today's market 🕒

Sumitomo Mitsui Financial Group Inc. Earnings (SMFG)

2:00 PM GMT: UMich Consumer Sentiment

Disney: Meet Brother Bear?

The Walt Disney Company (DIS) wanted investors to stop obsessing over its streaming subscriber growth and focus on revenue and profitability. True to the script, both metrics were below expectations in the recently concluded quarter. It also expects subscriber growth to taper. The result? Shares lost $20B in market value. Does the company find itself at crossroads?

Crown Captured, Cash Burnt

Disney launched its streaming service - Disney+, three years ago on November 12, 2019. By then, Netflix already had close to 160M subscribers, and the pandemic was just about to hit, which would send its numbers shooting through the roof and even cross 200M.

But Disney and Netflix had a straightforward differentiator - the former offered more options. Aside from the conventional Disney+, it also got sports content of ESPN+ and other streaming content from Hulu under its wing. Swifter launches, expansion to more territories, and investing heavily to acquire a subscriber meant Disney rapidly caught up with the crown.

Currently, the trio of Disney+, ESPN+, and Hulu have 235M subscribers, compared to Netflix's 223M. But people on the street are now talking of subscriber saturation within the streaming business. One would believe that theory on watching Netflix’s subscriber additions this year. However, Disney has no such problems as subscribers continue to pile on to its services.

On a standalone basis, Disney+ still has fewer subscribers than Netflix, but it added 12.1M new subscribers in the recently concluded quarter, compared to a paltry 2.4M for Netflix. Here comes the catch: Disney does not want you to focus on the number of subscribers it has for its streaming business. Instead, it wants you to focus on its revenue and profitability for the overall business.

Ironically, the metrics that Disney wants you to focus on ended up bringing about their downfall earlier this week. Both revenue and profitability missed expectations in Q4, with subscriber growth turning out to be the saving grace.

Key Highlights From Q4 FY22:

Revenue: $20.15B Vs $21.24B expected

Earnings Per Share: $0.30 Vs $0.55 expected

Disney+ Subscriptions: 164.2M Vs 160.45M expected

Revenue in the Media and Entertainment division declined 3% to $12.7B, much below the $13.9B figure analysts expected. Content sales were lower due to fewer theatrical films on the calendar.

Time To Stream Profits

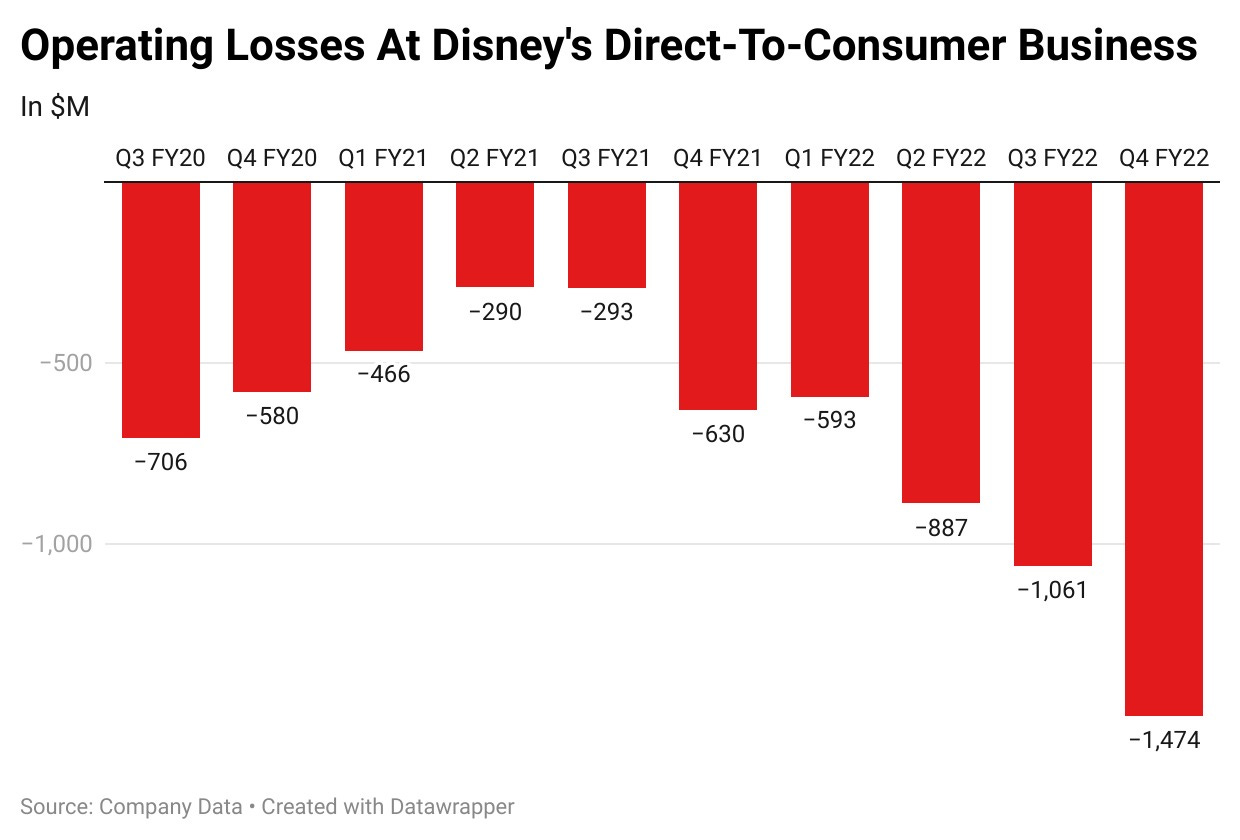

Subscriber growth may have been Disney's only solace during the quarter, but it has come at a massive cost.

The streaming business lost nearly $1.5B in Q4, double the same period last year and 38% higher than expectations. In the three years since its launch, Disney+ has lost $8B.

However, the management is unperturbed and expects the losses to improve by $200M in the current quarter and further reduce in Q2 of the next financial year. CEO Bob Chapek reiterated that the streaming business will turn profitable in the fiscal year 2024.

On the lines of Netflix, Disney+ will also launch an ad-supported tier worth $7.99 per month on December 8. It will also undertake substantial price hikes for the streaming division to focus on improving its revenue and profitability.

Are you still wondering why Disney wants you to focus on its revenue and profit when you can just be happy with healthy subscriber growth? It expects the latter to grow “only slightly” in the current quarter and that this strong growth trend may start to taper.

Disney+ will spend close to $30B on content next year but is looking to reduce expenditure in other areas, such as marketing. It expects high-single-digit growth in operating income and sales for 2023, lower than the 12% expectation on the street.

Of course, streaming is not the only business Disney has. Theme parks, which have long been the company's identity, reported record results in Q4. The Parks, Experiences, and Products segment reported 34% revenue growth to $7.5B, while operating income rose 66%.

Even the record results left analysts unimpressed. The $7.4B revenue was lower than their estimate of $7.5B, while the operating profit of the parks business at $815M was well below the $919M estimate. The parks business lost operating income worth $65M due to Hurricane Ian.

The ad tier has left the street divided. A group of analysts believes this would be more profitable than the traditional tier. In contrast, another group says that the ad tier, coupled with price hikes, may force some people to opt-out of the service, especially in these times of heavy inflation.

Disney lost $20B in market value in a single day after witnessing the biggest single-day drop in two decades. CEO Chapek knows that investors are running out of patience and that the streaming business must start delivering soon. For now, Disney has walked into the trap of its own words, and only the management can find a way out of it!

Market Reaction

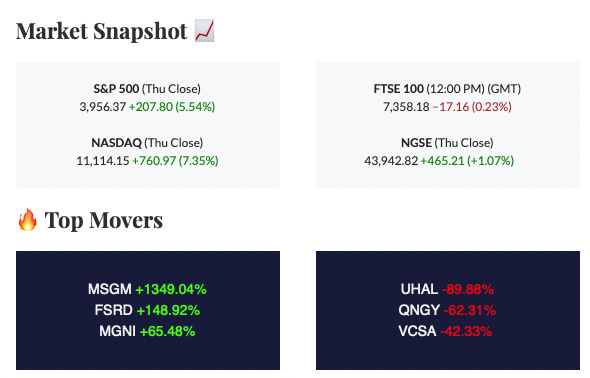

DIS ended at $90.46, up 4.28%.

Newsworthy 📰

New Avenue: Gap starts selling its apparel on Amazon after distribution deal with e-commerce giant (GPS +8.47%)

Measures: WeWork to close 40 US locations as the company cuts costs post wider-than-expected loss (WE +7.00%)

Worries: Apple supply crunch on premium iPhone threatens to derail record sales run (AAPL +8.90%)

What Next?

Subscribe to the Trove YouTube Channel

Join the Trove Telegram Community

Rate us on the Playstore or Appstore

Disclaimer: The email content is prepared and provided by Winvesta India Technologies Ltd. for informational and educational purposes only and is not meant to represent trade or investment recommendations. Remember capital is at risk. Terms & Conditions apply.